Credit scores evaluate the likelihood that you’ll repay a loan. They help lenders determine loan qualification, credit limits, and interest rates.

A credit score can be a mystifying number, but it’s an important number. Generally, you need a credit score of 600 to even qualify for a loan. Loans aside, you may need a good credit score to lease an apartment, amongst other things. You’ll also need to use a credit reference to be able to borrow money for a loan. A credit reference provides an overview of your credit history background and creditworthiness.

There are a few different types of credit scores that you can have, but the two most common credit models that are used to determine credit are VantageScore and FICO. It’s important to be aware of the typical score so that you can see how your credit score compares. The average credit score is around 675, but this differs by age and state.

So– how is a credit score calculated and what affects your credit score?

A variety of factors are taken into consideration. You should know them all so whenever a financial situation arises that mandates a credit check, you’ll have already worked toward building a high score.

In the previous chapters, we answered the questions “What is a credit score” and “Why do you need a credit score?” But in this chapter, we’ll examine the categories that are used by credit reporting agencies to determine your credit score, as well as credit score myths. Keep reading to find out more about what affects credit scores and what doesn’t.

- Payment History

- Age of Credit and Type of Credit

- Credit Utilization Ratio

- Total Balances and Debt

- Recent Credit Inquiries

- Available Credit

- What Doesn’t Affect Your Credit Score?

- Credit Score Myths

- A Summary: What Affects Your Credit Score

1. Payment History

Payment history is often the most heavily weighed factor that affects your credit score. Credit reporting agencies will check to see if you’ve been paying your debt on time. If you promptly make payments on all your accounts, you may earn a higher credit score. Consistently making late payments may result in a lower credit score.

It’s important to remember that late payments on rent or utilities will not affect your credit score—unless the issue has been taken to court. Credit reporting agencies are primarily looking at payments on debt: credit card payments, mortgages, auto loans, etc.

Credit reporting agencies may probe:

- How often do you pay late?

- When did you last pay an account late?

- How many days late have you made payments?

Unpaid debt may severely dent your credit score, especially debts that have been assumed by collection agencies. If you develop poor credit due to late payments, it’ll be more difficult to do things like purchase a car, qualify for a loan, or even make a down payment.

How influential is payment history?

Payment history is the most influential factor in determining your credit score. If you pay your existing debt promptly, then you’re more likely to pay your new debt promptly—that’s the way credit reporting agencies see it. Payment history is a strong, but not always perfect, indicator of whether you’re capable of responsible repayment.

How do I maximize my credit score in this category?

Make sure you pay your bills on time. Consider setting up automatic payments on debt so that you’ll never miss an installment or credit card payment. Paying your bills on time is a good credit habit to develop to ensure you never miss a payment.

What if I don’t have a long payment history?

Some people don’t have a very long history of debt payments; they’ve never taken out a loan or mortgage, they’ve never used a credit card, or they’ve only been making payments for a short period of time.

If you want to establish a history of prompt debt payment, consider opening a credit card. However, if you’re unable to open a credit card (due to a low credit score—which might be the result of a short credit history), consider building your credit by opening a store credit card.

Store credit cards aren’t weighed as heavily as bank credit cards, but they’re one way to prove your reliability in paying debts, and they may build your credit. Whether you open a bank credit card or store credit card, just remember to make your payments on time!

It takes time to develop a long payment history, but it’s helpful to be aware of how to build credit as a young adult so that you can get started as quickly as possible. We’ll be discussing various credit building strategies later on in Chapter 8 of this series.

2. Age of Credit and Type of Credit

The state of your current credit accounts is the second most influential factor that affects your credit score. Credit reporting agencies may evaluate:

- The age of your existing credit

- The types of credit accounts you have

Why does the age of my credit matter?

You might earn a higher credit score if you’ve regularly paid your debt over a long span of time.

Credit reporting agencies may see this as a future indicator; if—over a span of years—you’ve been prompt at paying off your debt, you’re more likely to do so in the future.

Credit age alone will not boost your credit score. If a credit account has been open for a while but you regularly make late payments, credit reporting agencies will see you as being more likely to make late payments in the future. That may result in a lower credit score.

Why does my credit type matter?

You might receive a higher credit score if you successfully maintain a mix of credit accounts: installment loans and revolving credit accounts.

Maintaining a mix of installment and revolving credit may demonstrate that you’re able to manage different types of loans.

Revolving credit demands a high amount of responsibility due to the varied amount of debt you may accumulate in a given month. A history of successfully managing revolving credit may result in a higher credit score.

How do I maximize my credit score in this category?

This is another difficult category for people who don’t have a long credit history.

Many people have student loans or auto loans, but not a revolving loan. Consider opening a credit card if you only have installment loans.

Be cautious about taking out an installment loan if you don’t truly need one. An installment loan will add to your overall debt, which also affects your credit score.

3. Credit Utilization Ratio

Credit utilization ratio measures the ratio of your credit card balance to your available credit limits. For example, if your credit card limit is capped at $1,000 per month, a balance of $500 in your account would make your credit utilization ratio 50%.

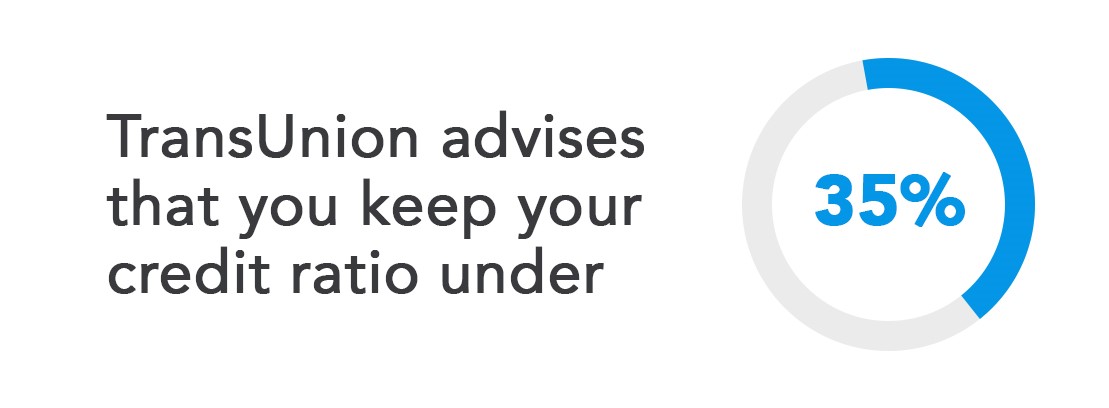

TransUnion advises that you keep your credit ratio under 35%. So, if your credit limit is capped at $1,000, you should use no more than $350.

How influential is credit utilization ratio?

Your credit utilization ratio is weighed just as heavily as Category #2.

A higher credit utilization ratio suggests that your balances are high. If your balances are high, there’s a greater likelihood that you’ll be unable to repay your debt.

A lower credit utilization ratio suggests that your balances are low. If your balances are low, there’s a greater likelihood that you’ll repay your debt on time.

How do I maximize my credit score in this category?

As suggested by TransUnion, you should keep your credit balances low. But beware of keeping your credit account too idle.

If you go some time without charging anything to your credit card, then credit reporting agencies will have no recent credit activity to draw upon, which won’t help your credit score increase.

If you have a revolving credit account, consider making a few small payments per month. You’ll keep your credit balance low, but you’ll also provide credit reporting agencies with activity to evaluate. If you pay off mild balances promptly and recurrently, you may receive a higher credit score.

4. Total Balances and Debt

Credit reporting agencies will evaluate the total amount of debt that you owe. Higher amounts of debt may result in a lower credit score, while less debt may result in a higher score. It’s important to be aware of the meaning of debt to credit ratio, which is the amount of debt you owe compared to your available credit. You need to have a low debt to credit ratio in order to improve your credit score.

How influential are total balances and debt?

This is a moderately influential category—not weighed as heavily as Category #2 and Category #3, and definitely not as much as Category #1.

If you have a substantial amount of debt, there’s a greater likelihood that you’ll be unable to take on new debt. That’s why higher debt negatively affects your credit score.

But large amounts of debt are not always an indicator that repayment is less likely—and that’s why this category is not weighed as heavily as the prior categories.

Someone could have a substantial amount of debt to repay, but if that person consistently makes payments on time—and over a moderate span of time—it may suggest that person is quite capable of prompt repayment.

Credit reporting agencies do not take a person’s income into account when determining that person’s credit score. Someone with a substantial amount of debt might also have a high income, and thus be very capable of making prompt payments. For that reason, too, this category is not weighed as heavily as the prior ones.

How do I maximize my credit score in this category?

Reducing your overall debt may result in a higher credit score. You can reduce the overall debt you owe by paying off your loans. Consider paying off installment loans first. When making payments on installment loans, you could contribute more than the required minimum so that you’ll pay off the loan faster.

If you’re heavily burdened by revolving credit debt, you might consider taking out an installment loan to help pay it off. Your debt wouldn’t immediately be reduced, but you could have your payments reorganized into smaller increments that are easier to pay. Remember that consistent, on-time payments may reflect well on your credit score. You don’t want unpaid revolving debt to accumulate—that may decrease your credit score.

5. Recent Credit Inquiries

Credit reporting agencies will evaluate whether you’ve made any recent “hard” inquiries. Inquiries occur when you get an evaluation of your credit score from a credit-reporting agency. There are two kinds of inquiries.

A soft inquiry is when you request an evaluation of your credit score without actually applying for new credit. For example, you might need your credit score to lease an apartment, or maybe you’re only trying to monitor changes in your credit score.

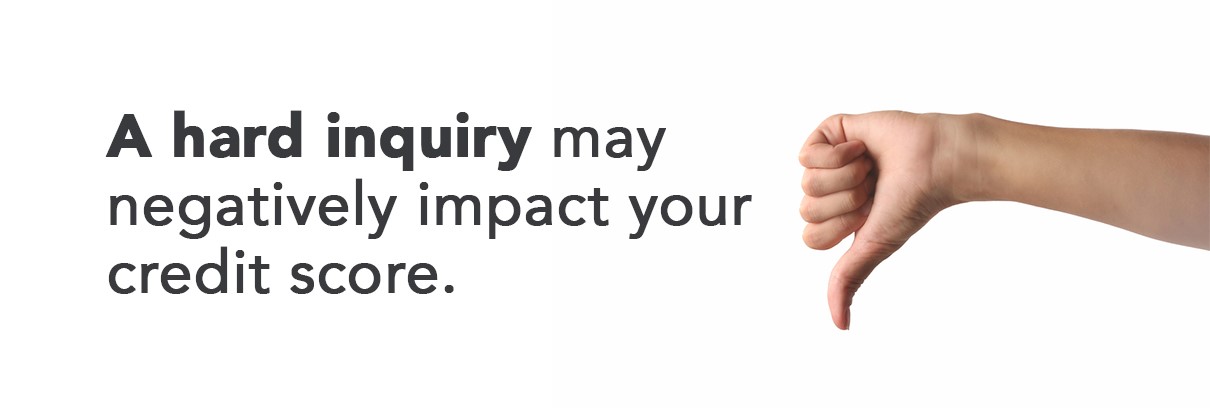

A hard inquiry is when you request your credit score for the purpose of applying for new credit—for a mortgage, new credit card, etc.

A hard inquiry may drop your credit score.

When you’re applying for new credit, you’re taking on new debt. By having debt, you naturally have more risk—that’s why your credit score may drop. Most hard inquiries, though, will only drop your credit score by a few points.

A soft inquiry will not affect your credit score.

How influential are recent credit inquiries?

This is a less influential category in determining your credit score. Just because you’re acquiring new debt, doesn’t necessarily mean you’re less capable of timely repayments. And you might even be opening new credit because you’re in a good financial situation to do so. For that reason, hard inquiries are not a heavily weighted factor.

However, opening too many new credit accounts may drop your score significantly.

Too many new credit cards and loans greatly increase the likelihood that you’ll overextend yourself and get behind on payments, or default.

How do I maximize my credit score in this category?

Avoid opening too many new accounts, and only open accounts that you truly need.

If you must open new credit accounts, try to apply for them all within a short span of time. You don’t want new credit accounts to be counted as separate hard inquiries—that may drop your credit score. But when inquiries are made within a short span of time, credit reporting agencies will do something called deduplication, where multiple hard inquiries of the same type are merged into a single inquiry.

VantageScore allows 14 days for deduplication. For example, if you were opening a new credit card, taking out a mortgage, and applying for an auto loan, you’d want to submit all applications within 2 weeks so they’d be counted as one inquiry.

6. Available Credit

Credit reporting agencies will examine how much revolving credit you have available that you haven’t used.

Available credit is related to credit utilization ratio. The credit utilization ratio primarily measures your credit account balance. Available credit measures the unused credit—as opposed to your used credit.

A large amount of available credit suggests that your finances are more stable because you have lots of breathing room.

However, “breathing room” doesn’t necessarily indicate that someone is unlikely to make timely repayments. For example, someone might have a small amount of available credit, but they also might have a near-flawless history of debt repayment. For that reason, available credit is not weighed very heavily and is a less influential category in determining your credit score.

How do I maximize my credit score in this category?

As discussed in Category #3, you could try to keep your revolving credit debt under 35% of your available credit. A larger amount of available credit may increase your credit score.

Be advised that some lenders may have limits on the amounts of available credit or open accounts you have, and if you exceed those limits, they may decline your application for a new credit account.

Consider opening only the amount of credit that you truly need.

What Doesn’t Affect Your Credit Score

So you now know what impacts your credit score, but what about what doesn’t impact your credit score?

A variety of personal details will have no impact on your credit score, like:

- Race

- Religion

- Gender

- Nationality

Other non-factors include:

1. Age

Many people think that age affects your credit score evaluation. But it’s credit history—not age—that affects your credit score.

It’s true that younger people are more likely to have a shorter credit history, but even older adults may have a short credit history if they’ve never taken out a loan or used a credit card.

Age itself is not factored by credit reporting agencies.

2. Marital Status

Married couples do not share credit scores; each spouse maintains their own.

If a married couple shares a joint credit account, however, one’s credit behavior may affect the other. For example, if one spouse makes a late payment, the other spouse who shares the account may also get penalized for it on his or her credit score. Bad credit in a marriage is something you should be aware of as it can have an impact on your own financial health.

3. Employment

Credit scores are not affected by your employment status, employer, occupation, or income. None of these factor into your creditworthiness. High income and employment factors are no indicator that debts will be repaid in a timely manner.

4. Assets

Your total assets are also not an indicator of timely debt repayment.

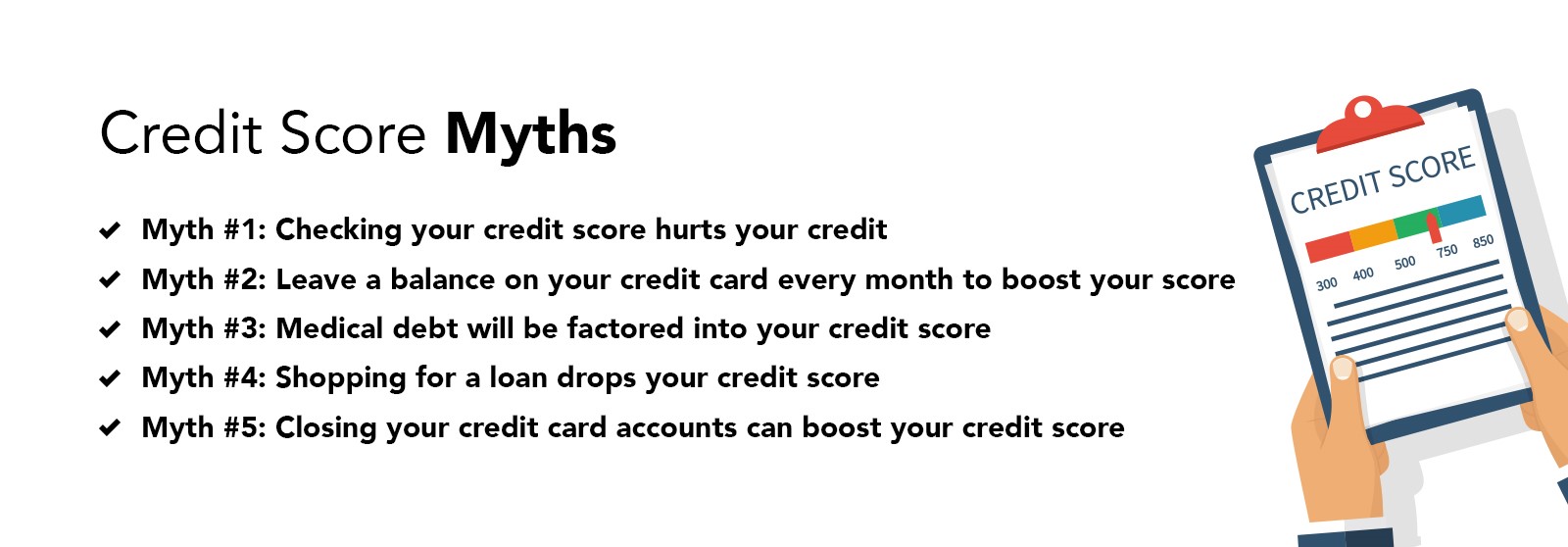

Credit Score Myths

There are some important things that affect your credit score, but there are also many factors that are irrelevant. In fact, there are many widespread myths about what boosts or drops your credit score. Let’s address a few of the most popular myths.

Myth #1: Checking your credit score hurts your credit.

A hard inquiry may drop your credit score, but hard inquiries only occur when you submit applications for new credit accounts. A soft inquiry does not affect your credit score.

You can get your credit score from credit reporting agencies even if you’re not applying for new credit, and this counts as a soft inquiry. Your credit score won’t be penalized for a credit check. In fact, consumers are encouraged to regularly check their credit score or have it monitored.

Checking your credit score regularly is important so that you can have a better idea of your financial standing. It’s also important so that you can catch potential fraudulent activity or incorrect information.

If you notice incorrect information on your credit report, be sure to follow the credit dispute process to get it removed before it can impact your credit score. You can stay on top of your credit history with a free credit score report, which you can get once a year.

Myth #2: Leave a balance on your credit card every month to boost your score.

Many people believe that if you leave a single balance unpaid, you’ll build your credit score faster.

This is untrue. You can build your credit score by paying your debt in full every month, or by keeping your balances as low as possible if you can’t.

Myth #3: Medical debt will be factored into your credit score.

Medical debt is not factored into your credit score unless it has been assumed by collections.

Myth #4: Shopping for a loan drops your credit score.

A hard inquiry might drop your credit score by a few points. But consumers are encouraged to look for the best loan rates possible. As discussed in Category #5, VantageScore has a 14-day window where all inquiries are deduplicated. So long as you submit loan applications within this window, you won’t be penalized for multiple hard inquiries.

Myth #5: Closing your credit card accounts can boost your credit score.

You may think that fixing closed accounts on your credit report can improve your credit score, but that’s not always the case. Closing your credit cards may actually drop your credit score.

Older revolving credit accounts are likely to boost your credit score, so long as you’ve managed them responsibly. On the contrary, your credit score may drop when you open new credit accounts. Thus, you want to keep revolving accounts open for as long as possible.

Additionally, closing a well-managed credit card means you won’t benefit from the credit utilization ratio. Closing an account might increase your balance-to-limit ratio, which may result in a lower credit score.

If a credit card has numerous late payments and mismanagement attached to it, closing the card won’t instantly remove those blemishes from your credit report. It might take years for credit reporting agencies to remove those accounts.

Rather than closing a credit card account, it may be better to keep the account open and benefit from its aging and credit utilization ratio. You could work to improve a record of late payments with timely payments.

Closing a credit card account might be a necessity for you under certain circumstances. Just be sure to have the numbers crunched so that you’re aware of how your credit score might be affected. Monitoring your credit score might help you avoid drastic changes when you’re considering such options as closing an account.

A Summary: What Affects Your Credit Score

At first glance, it might seem like the VantageScore categories that credit reporting agencies use to determine your credit score are rather dense and complex.

But a disciplined adherence to a few principles may go a long way in boosting your credit score with ease.

One of the most important rules to follow is:

- Make debt payments on time.

This is the most heavily weighted factor in determining your credit score. If you must, set up automatic payments so that you’ll never miss one.

In addition, you may be able to boost your credit score by:

- Maintaining a variety of credit accounts—to supplement installment loans, open a credit card and make small charges on it each month. Be sure to pay those balances in full.

- Let your credit accounts age, and don’t open new ones unless you have to.

- When you open multiple new accounts, submit all applications within 14 days so you can deduplicate inquiries.

- On revolving credit accounts, try to keep your balances under 35% of your available credit limit.

- Reduce your debt as much as you can. Try and pay off any installment loans, and contribute more than the required amount each month.

By being aware of what affects your credit score, you might be on your way to building a high credit score.

In the next chapter, we’ll discuss what the credit score ranges are, so you can understand where your credit score falls and what that means.

Sources: Experian | FICO 1 2 | TransUnion

Comments

Post a Comment

We will appreciate it, if you leave a comment.