Student loan forbearance is a temporary suspension or decreased rate on your student loans. Many people became familiar with student loan forbearance during the COVID-19 pandemic, during which many student loan payments were halted or cut.

Navigating student loans can be a tricky business as it is. But if a lower interest rate piques your interest, we’ve put together a guide to what student loan forbearance means and how it works.

What is Student Loan Forbearance?

Student loan forbearance means you’ll get some reprieve from your loan payments for a time. This could mean your monthly payment is reduced or even stopped altogether for up to one year.

For the most part, forbearance isn’t an automatic process. You’ll have to contact your loan provider and fill out a form to request it. From there, your provider will determine whether or not to grant you forbearance.

Let’s break down the different types of loan forbearance.

General Forbearance

General forbearance, also called discretionary forbearance, is the most common type of student loan forbearance. Under this model, a person who thinks they qualify for forbearance contacts their loan provider, who will either approve or deny their request.

A few reasons people might request general forbearance include:

- Job change

- Medical bills

- Financial crisis

In some situations, other financial crises will make someone eligible for loan forbearance. If you think you might be eligible, contact your loan provider.

Mandatory Forbearance

In some cases, the loan provider is required to grant the lendee forbearance. If you can provide the necessary documentation to prove you qualify, your provider will be legally obligated to grant your request.

A few reasons people might request general forbearance include:

- High payment to income ratio

- Qualifying job or residency

- Military status

While you will still have to contact your loan provider and apply for forbearance, your lender is required to give you some form of relief.

Private Forbearance

Forbearance is generally only an option under federal student loans. However, those who have privately-funded loans may still be able to apply for it. If you have private loans, contact your provider to learn about their policy on forbearance.

Pros and Cons of Student Loan Forbearance

| Pros of Student Loan Forbearance | Cons of Student Loan Forbearance |

|---|---|

| Prevents you from defaulting on your loans | Usually only lasts 12 months |

| Doesn’t impact your credit score | Accrues interest over time |

| Gives you time to become financially stable | May require an upfront payment |

Loan forbearance is typically only sought after and granted to people who experience financial hardships. Because of this, the biggest pro of forbearance is that it can give you time to get back on your feet and start paying down your loan. However, forbearance may have some cons compared to other loan easement options, as it will continue to accrue interest.

Alternatives to Forbearance

Those who aren’t interested in forbearance have other options. Your loan provider can help you navigate which will be right for your needs and lifestyle.

Some potential options are:

- Switching your payment date to a more convenient day

- Getting a debt consolidation loan to combine all your payments into one

- Applying for loan forgiveness

- Refinancing your loans

Your loan provider can help you navigate your options and determine which will be the best for your financial needs.

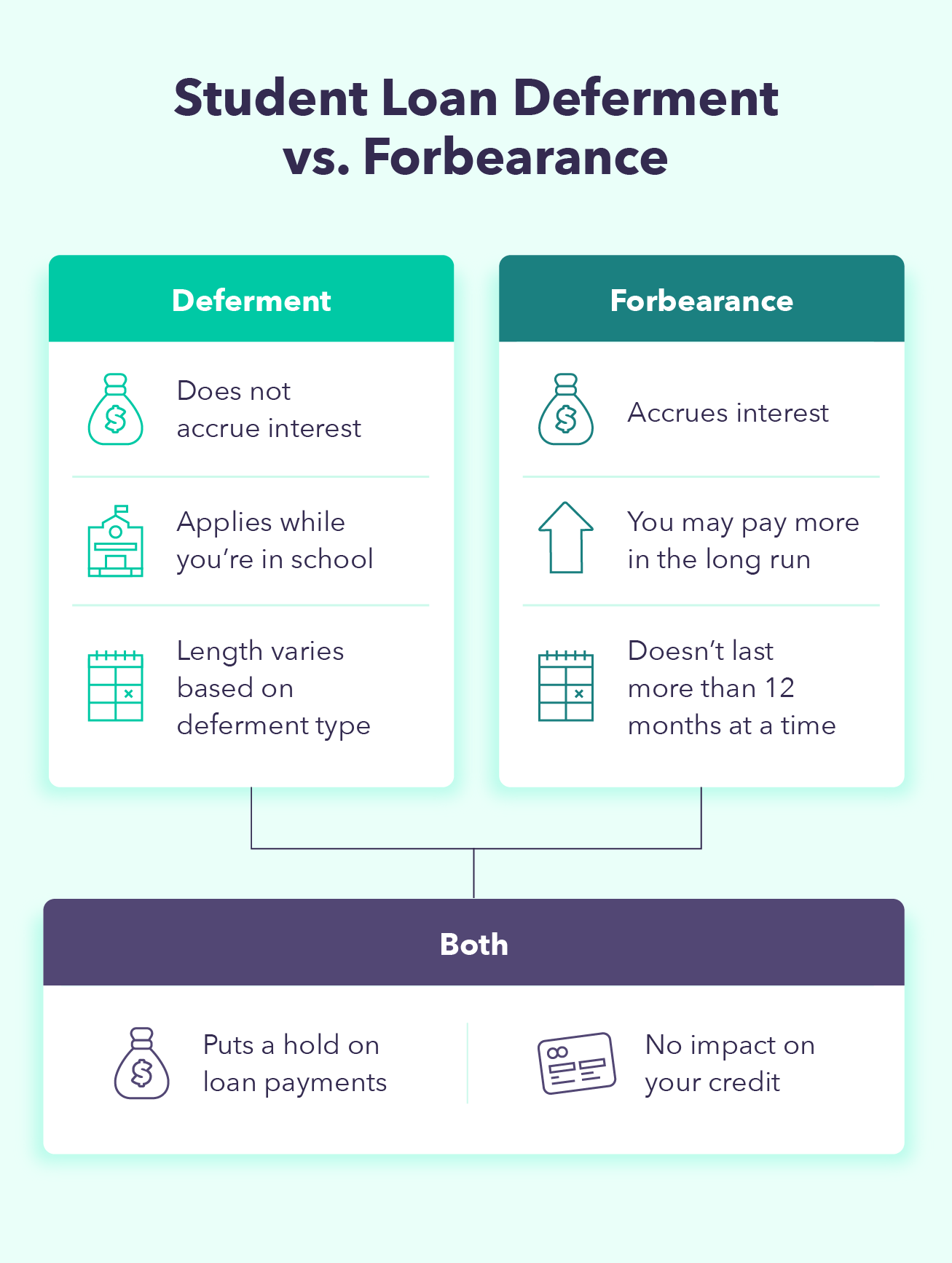

Deferment vs. Forbearance

Another popular option is loan deferment. While both forbearance and deferment will allow you to delay your loan payments, there is one key difference: interest. If your provider grants you loan forbearance, your loans will still accrue interest over time, which means you’ll end up paying more. If you are granted loan deferment, your loans will not accrue interest.

The Bottom Line

Those who find themselves in hot water may be able to cool down with student loan forbearance. This 12-month grace period can allow you to set up a budget and get back on your feet before starting up payments again.

Whether or not student loan forbearance is an option — or the terms of your forbearance — is up to your loan provider. That’s just another reason why finding the right student loan for you is of the utmost importance.

Student Loan CalculatorFAQs about Student Loan Forbearance

Have some more questions about loan forbearance? We have answers.

While student loan forbearance may not be ideal, it isn’t bad. It’s certainly better than the alternative—defaulting on your loan. The main drawback of student loan forbearance is that your loans will continue to accrue interest and can be expensive in the long run.

If your loans are in forbearance, it will prevent you from getting your loans forgiven. In order to apply for (and be granted) student loan forgiveness, you need to be actively making payments on your loans

People may qualify for student loan forbearance for a variety of reasons. For example, someone who has just changed jobs and needs time to adjust may be able to apply for forbearance. Veterans, teachers, those in a medical residency program, or someone with high medical bills may also qualify.

If you think you’re experiencing qualifying financial hardship, contact your loan provider.

The post Student Loan Forbearance: A Definition and Overview appeared first on MintLife Blog.

from MintLife Blog https://ift.tt/0hmWuzD

Comments

Post a Comment

We will appreciate it, if you leave a comment.