With 59 percent of adults in the U.S. living paycheck to paycheck, many people struggle to have fun while still paying for their necessities. After all, it’s hard to spend money on yourself when you’re under financial stress. But creating a fun money budget can help you have a good time with any budget.

To keep your spending under control, make a budget and set aside some money each month to spend on things you want—sans guilt with no strings attached. This can help you create a healthier lifestyle that’s full of fun without sacrificing your financial goals. And this guide can teach you how to do all of this and then some. Without further ado, let’s save some fun money.

What Is Fun Money?

Fun money is money you budget to spend on your wants (rather than your needs) each month. A fun money budget keeps you on track to meet your long-term financial goals while still giving you the freedom to spend on items and experiences that enrich your life.

Think about it as Marie Kondo-ing your budget. Does this expense spark joy? If your answer is yes, that’s an expense from your fun money budget.

Many people feel guilty spending money on things or experiences they enjoy if they’re not necessities, but you shouldn’t have to! Budgeting fun money empowers guilt-free spending while staying on course to meet your financial goals.

For instance, you might use a fun money budget to save up for and enjoy things like:

- Concerts

- Travel

- Spa days

- Restaurants

- More

Fun money gives you the freedom to enjoy experiences you might have otherwise denied yourself due to financial anxiety or guilt. It also helps you prioritize your finances to make responsible decisions about where to spend and where to save, so you’re not tempted to max your credit card the next time your favorite band tours.

Fun money budgets work because they’re a fiscally-responsible way to have fun. When you take care of necessities first, then you don’t need to worry about making sacrifices and missing out on fun. Fun money isn’t permission to spend all your money on wants—it’s a smarter way to budget for fun.

Why Is Fun Money Important?

Fun money can be helpful for maintaining your mental health while you’re paying off debt. You’re much more likely to get financial burnout if you punish yourself every time you grab a latte versus if you don’t let yourself spend money on things you enjoy.

All this to say, everyone deserves to have fun, but it’s hard when you’re stressed about making ends meet. That’s why fun money is important for the following reasons.

1. Fun Money Helps Stop Overspending

People aren’t as aware of their budget as they think—in fact, only 35 percent of Americans know how much they spent in the last month. If you have no budget at all or a restrictive budget because of debt (which almost every American does), then you’re actually more susceptible to overspending.

If you never let yourself spend money on fun, you’re bound to break eventually then go overboard, thinking, “Well, I never spend money on X, so I can splurge now.” This impulse decision is called emotional spending.

Fun money either gives you a safe fund to splurge from or prevents those split-second bad decisions because you know if you pass on this fun opportunity, you’ll get another chance.

2. Fun Money Makes Budgeting Enjoyable

Let’s be honest, budgeting isn’t exactly the most fun way to spend your afternoon. But budgeting is a lot easier when you’re certain it’s going to ensure you have more fun.

It’s easier to sit down and work out a budget when you know there’s a light at the end of the tunnel—hello, fancy dinner at your favorite restaurant. Otherwise, saving for the future can feel pointless because you’re sacrificing too much in the present.

Fun money helps you reframe your spending to make budgeting and spending a positive experience. When you know that you’ve taken care of your necessities, you can have carefree fun and build a positive relationship with your finances.

3. Fun Money Prevents Spending Guilt

A fun money fund helps take some of the mystique out of spending money on what you enjoy. How many times have you saved up for something, only to feel post-purchase guilt because you worry that money should’ve gone to a necessity?

Spending guilt also leads to a phenomenon called “spaving.” Basically, you spend more money than you would have originally for the sake of scoring a deal. Buying in bulk is tempting, but sometimes it doesn’t make sense to have 50 rolls of toilet paper stashed just to save a couple dollars.

Everyone experiences spending guilt from time to time, but as long as you’re not withdrawing emergency funds or neglecting your bills, there’s no reason to feel bad about treating yourself.

4. Fun Money Brings Surprising Health Benefits

Many Americans suffer from financial anxiety. In fact, over 30 percent of Americans regret spending as much as they did in the last month.

It’s common to struggle with financial guilt and anxiety when you inevitably decide to have a day out with friends or buy that sweater you’ve had your eye on. Long-term, this pattern of thinking leads to a scarcity mindset.

A scarcity mindset is when you’re so focused on what you don’t have that you neglect the things you do. When you start setting up a fun money budget, you give yourself permission to enjoy the things you have and combat this negative mindset.

A fun money budget might help alleviate feelings of financial anxiety. The key is to budget safely, so you know that even if you’re spending all your fun money, your basic needs will still be met. It takes some time to adjust, but soon you’ll be able to enjoy fun purchases guilt-free and lessen your financial anxiety.

How to Budget for Fun Money

Different budgeting strategies work best for different people and different financial goals. As long as your basic needs are met and you have some room to have fun, consider yourself a successful budgeter. Let’s look at some common budgeting strategies if you’re unsure how to get started budgeting for fun money.

Zero-Based Budgeting

Zero-based budgeting involves creating a detailed report of your expenses to have a very precise idea of your monthly budget. Basically, you decide where each dollar you earn is going ahead of time.

While this takes more effort upfront, once you have your budget in place, you’ll have a much better understanding of your finances. To determine your zero-based budget:

- Write out all fixed expenses and total their costs.

- Write out all variable expenses and total their average costs over the past 2–3 months.

- Deduct fixed expenses and average variable expenses from your monthly take-home.

- Divide the remaining amount between savings/financial goals and fun money.

Zero-based budgeting is a good option for people who feel like they’re not in control of their finances because it shows you precisely where all your money is going each month.

50/30/20 Rule

The 50/30/20 method is a way to break up your monthly income so you know how much you should be spending on needs, wants, and necessities. To follow this method, allot your monthly take-home income like this:

- 50 percent to your needs

- 30 percent to your wants (AKA your fun money)

- 20 percent to your savings and debt payments

The 50/30/20 rule is a good tool for planning out future purchases or determining if you’re already overspending.

To determine if you need a budget reality check, multiply your monthly take-home amount by 0.3, which will give you 30 percent. Then see how this number compares to what you’ve been spending on your wants for the last couple of paychecks.

The 50/30/20 rule is a good starting point for people who feel overwhelmed by the idea of budgeting and want to keep their finances simple.

Pay Yourself First Method

When you pay yourself first, you take care of your necessities as soon as you get paid and spend the rest of your income on your wants. With this method, you don’t need to stress about pulling your budget together at the end of your month because your needs will be taken care of. Then you can focus on your financial goals and fun money.

To determine how much you should put away for your financial goals:

- Make a list of goals and a timeline for reaching them.

- Divide the total amount you need to save for each goal by the amount of time (in months) you have given yourself to reach them.

- Add up the amount you should pay each month for your goals.

To pay yourself first:

- Calculate your monthly income.

- Deduct the money you spend on your needs from your monthly income.

- Deduct what you’re saving for financial goals from your monthly income.

- Enjoy the leftover fun money guilt-free.

Try paying yourself first if you feel most stressed at the end of the month. This way, if you’re feeling a little short on cash, you know your basic needs are already taken care of.

Fun Things to Spend Money On

The whole point of a fun fund is to spend money on things that bring you joy. If you’ve been restricting yourself for a while, you might be overwhelmed and not sure what to do with your fun money. Here are some tips for fun at any budget.

Free Activities:

- Host a themed movie night

- Challenge a friend to a cooking contest with ingredients you already have

- Head to the library to discover your new favorite series

Low-Cost Activities:

- Invite friends over for a potluck

- Host a sip and paint or arts and crafts night

- Learn a new hobby or skill

Mid-Cost Activities:

- Set a budget for a mini-shopping spree

- Go out to dinner at a new restaurant

- Attend a play or concert

Splurge Activities:

- Schedule a weekend trip

- Spend a day at the spa

- Sign up for cooking classes

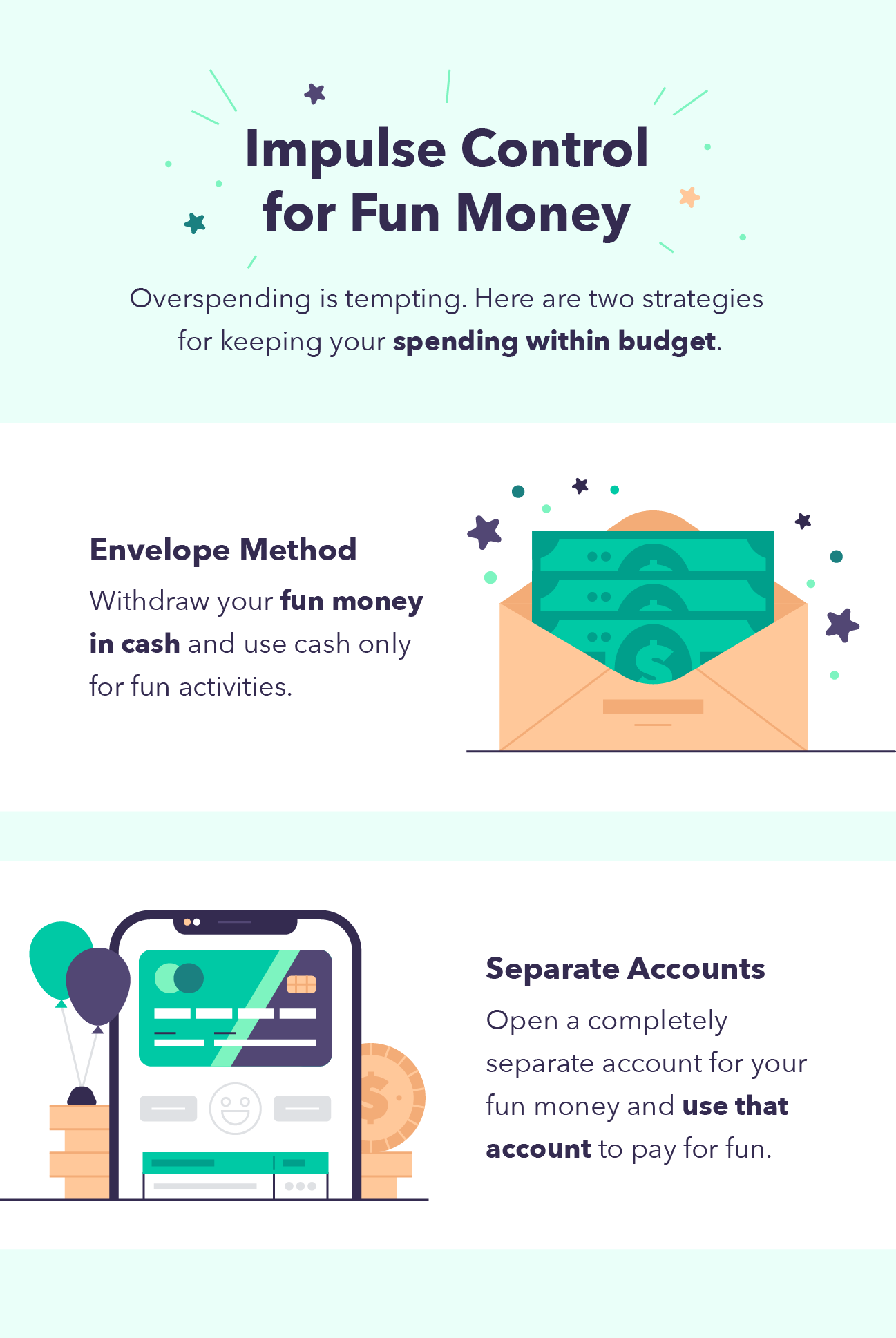

Tips to Stop Impulse Spending

Even with a fun money budget, some people may have trouble restraining themselves and continue to overspend. While you adjust to your new budget, try these strategies to keep your spending within budget.

Try the Envelope Method: For the envelope method, withdraw your fun money in cash each month and keep it in an envelope. Each time you go out for a non-essential reason, limit your spending to just the cash from that envelope so you don’t overspend.

Make a Fun Money Bank Account: If you’re not into carrying around cash, try opening a separate checking account for your fun money budget. Use only this debit card when you’re making purchases and turn off overdraft capabilities to keep yourself in check.

How Much Should Your Fun Money Budget Be?

Everyone’s income and expenses are different, so there’s no hard rule as to how you should split up your budget. Once your basic expenses are covered, it’s up to you to decide how to divide your remaining income between financial goals and fun.

Don’t be discouraged if your fun money fund is a little less than you’d like—there are plenty of ways to make that money stretch. For example, host a mixology contest instead of heading to a bar save you money without compromising your fun.

The Bottom Line

It’s not worth it to burn yourself out because you’re not letting yourself spend money on anything fun. That’s why it’s so important to set aside fun money to make sure you’re letting yourself have fun while saving to meet your financial goals.

Try out a fun money budgeting strategy with your next paycheck to help keep you on track so you can live your life without sacrificing the necessities. And when in doubt, consider a budget app like Mint to keep your finances fully organized.

Comments

Post a Comment

We will appreciate it, if you leave a comment.