Is there a portfolio that will enable you to money every year and in all economic, financial, and market environments? Unfortunately, not. But one portfolio strategy – Ray Dalio’s All-Weather Portfolio – offers something all investors will welcome: the potential of positive returns in years when growth-oriented investment strategies are in steep decline.

That’s hardly a surprise when you consider that the All-Weather Portfolio’s primary founder, Ray Dalio, is the chief investment officer for Bridgewater Associates, the largest hedge fund in the world. Hedge funds, after all, are in the business of mitigating risk. That comes in mighty handy when the financial markets are misbehaving.

And that’s exactly what makes the All-Weather Portfolio so interesting.

Table of Contents

- What Is the All-Weather Portfolio?

- Who Is Ray Dalio and What Is Bridgewater Associates?

- How the All-Weather Portfolio Works

- Investment Allocations for Each of the Four Market Environments

- All-Weather Portfolio Performance When It Matters Most

- How to Create Your Own All-Weather Portfolio

- Other “All-Weather Portfolios”

- Should You Invest In the All-Weather Portfolio?

What Is the All-Weather Portfolio?

Typical growth-oriented portfolios are designed to produce significant returns during periods of stability, growth, and general prosperity. But they can reverse dramatically during times of economic and financial distress.

For example, the NASDAQ Composite stock market index, which performed so well throughout the 1990s tech boom, experienced a 78% decline during the Dot-com Bust from March 2000 through October 2002. That’s the kind of decline that not only destroys portfolios but often turns investors into non-investors.

The All-Weather Portfolio is designed to thrive in exactly such tumultuous market environments. By maintaining specific mutually exclusive asset allocation – some would even call them boring – the All-Weather Portfolio doesn’t just preserve portfolio value but enables it to grow.

That’s a feature that should get every investor’s attention.

Who Is Ray Dalio and What Is Bridgewater Associates?

As mentioned earlier, Ray Dalio is the founder, co-chairman, and co-chief investment officer at Bridgewater Associates, the world’s largest hedge fund. Based in Westport, Connecticut, the fund has $140 billion in assets under management. Its clients are large institutional investors, like governments, corporations, and pension funds, looking to generate more predictable, long-term returns.

Dalio and the firm came to prominence primarily on the strength of the All-Weather Portfolio. They successfully sold the concept of protecting portfolios from declines during falling markets – a popular concept among institutional investors, who need consistent returns to meet portfolio obligations, like pension payments. Predictable 5% to 8% annual returns are more valuable than a 30% gain one year, followed by a 25% loss the next.

The All-Weather Portfolio was formalized in 1996 and has enabled Bridgewater Associates to become the world’s largest hedge fund.

How the All-Weather Portfolio Works

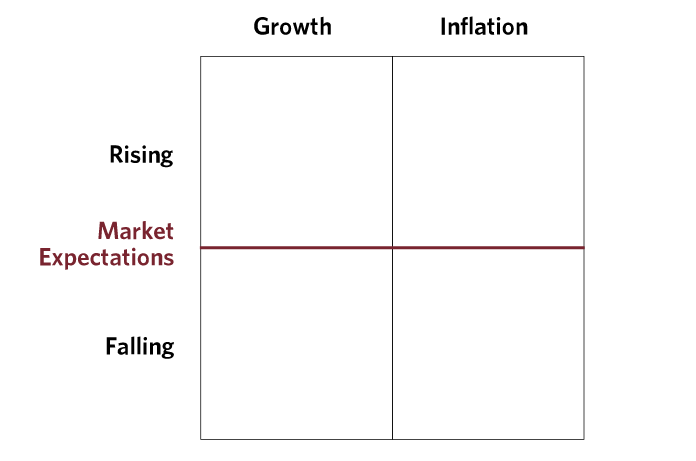

The basic concept of the All-Weather Portfolio isn’t to perform brilliantly in a particular market but to perform positively in all types of markets.

The All-Weather Portfolio looks beyond the single market environment favored by most investment strategies – stability, growth, and general prosperity.

Dalio and his team recognize four distinct investment environments, characterized by the following grid:

Typical growth-oriented investment strategies focus on the upper left quadrant, rising market expectations, and growth. Over the long run, this strategy often produces explosive returns, great enough to offset losses in the down years.

But it requires strict adherence to a buy-and-hold strategy. The investor must be fully prepared to hold onto the designated portfolio, even when values are crashing.

But buy-and-hold is limited by human emotion and psychology – as well as personal financial circumstances.

It can be tough to hold onto a portfolio that has already declined by 30%, 40%, 50%, or more. Many investors reach their risk tolerance point well into a decline when losses are significant. Those losses can take many years to overcome because the investor may become risk-averse for several years and miss out on the best returns in the next bull market.

Since rapidly deteriorating financial markets are closely correlated with weak economies, investors may need to liquidate assets to survive, particularly after a job loss.

Human emotion tests the theory of buy-and-hold and endurance during severe declines.

The All-Weather Portfolio avoids this dilemma because it’s designed to outperform when markets decline. That includes periods of rising inflation and falling market expectations, increasing growth and growing inflation, and decreasing growth and falling inflation (deflation).

Investment Allocations for Each of the Four Market Environments

While it’s easy to identify investment opportunities in times of rising growth and market expectations, the difficulty is in finding those for the other three market environments. That’s what the All-Weather Portfolio can do.

The All-Weather Portfolio uses the following model:

(EM Credit = emerging market credit; IL Bonds = inflation-linked bonds, like TIPS; nominal bond = regular bonds that have no inflation provision.)

Notice that the grid assigns equal weight (25%) to each of the four investment environments – not because each is likely to occur with the same frequency, but because the occurrence of any is entirely unpredictable.

In other words, the All-Weather Portfolio is prepared for any environment at any time. This is a critical adaptation because it’s usually not known when one market environment has shifted into another until well after the fact. The All-Weather Portfolio is designed to work within the framework of this uncertainty.

The key components and asset class weights of this strategy are:

- 30% in U.S. stocks

- 40% in Long-term U.S. Treasury Bonds

- 15% in Intermediate-Term U.S. Treasury Bonds

- 7.50% in Gold

- 7.50% in broad Commodity basket

All-Weather is an advanced portfolio allocation strategy. Nominal bonds protect principal in a falling stock market while offering the potential for increased values in a market that features negative inflation and falling market expectations, think 1930’s deflation. The position in US stocks is primarily to react to a period of growth with rising market expectations.

But during rising market expectations and inflation, gold, commodities, and inflation-linked bonds could provide positive returns. (Inflation-linked bonds are essentially Treasury Inflation-Protected Securities (TIPS) issued by the US treasury. They can be included in both the long-term U.S. Treasury bonds and intermediate-term U.S. Treasury bonds allocations since TIPS are available in terms of five, 10, and 30 years.)

It’s the asset mix that gives the All-Weather Portfolio its staying power in virtually any type of market. And it shows in the consistency of the portfolio’s performance.

All-Weather Portfolio Performance When It Matters Most

In most years, the All-Weather Portfolio will easily be outperformed by the S&P 500. But the portfolio isn’t designed to keep up with the S&P 500. Its primary purpose is to provide positive returns during times of market turmoil.

By that standard, the All-Weather Portfolio has lived up to its promise.

Between 2003 and 2021, the portfolio produced positive returns in 17 of 19 years. The only losses were in 2015 and 2018, when it returned -3.72% and -3.19%, respectively. The portfolio’s best performance was in 2019 when it returned 18.22%.

Of more interest is the return during the Financial Meltdown that began in 2007. Those returns looked like this:

- 2007: +11.88% (S&P 500: +5.48%)

- 2008: +1.34% (S&P 500: -36.55%)

- 2009: +2.34% (S&P 500: +25.94%)

This was a significant performance because the All-Weather Portfolio provided positive returns during a nearly three-year timeframe that was the worst financial market in recent memory.

Notice that the portfolio outperformed the S&P 500 in 2007 and 2008. Though the S&P beat it in 2009, it spared investors losses in each of the three affected years.

What about 2020, the year of the coronavirus crisis?

Though the S&P 500 turned in an impressive 18.01% return for the year, the All-Weather Portfolio returned 14.68%. That may be less than the S&P 500, but the All-Weather Portfolio offered exposure to income while turning in a very healthy double-digit return in a crisis environment.

How to Create Your Own All-Weather Portfolio

If you want to create an All-Weather Portfolio, you can use ETFs that most closely represent the asset classes recommended for the portfolio.

In the past, NASDAQ has recommended the following funds:

- 30% Vanguard Total Stock Market ETF (VTI)

- 40% iShares 20+ Year Treasury ETF (TLT)

- 15% iShares 7-10 Year Treasury ETF (IEF)

- 7.50% SPDR Gold Shares ETF (GLD)

- 7.50% PowerShares DB Commodity Index Tracking Fund (DBC)

Just as the All-Weather Portfolio is reliable in the most unreliable market environments, it’s also straightforward to create. Five funds are all it takes. By including these five funds in your portfolio and the recommended allocations, you can create an All-Weather Portfolio for yourself.

Other “All-Weather Portfolios“

The All-Weather Portfolio isn’t the only all-weather portfolio concept. Here are some alternatives.

The Permanent Portfolio

In 1982, Harry Browne founded the concept of the Permanent Portfolio, which has become an actual fund. The Permanent Portfolio works by maintaining equal (25%) allocations in each of four asset classes: growth stocks, gold, long-term U.S. Treasury bonds, and short-term U.S. Treasury bills.

The allocations have been modified somewhat over the years, and the current makeup of the fund is as follows:

Since its inception in 1982, through 2020, the Permanent Portfolio’s average annual return is 6.55%; that’s below the S&P 500 index, but the S&P has been invested in a high-performing single asset class over the same period.

The real strength of the Permanent Portfolio is its performance during crisis years. For example, the portfolio has the following returns during times of financial upheaval:

1987 – stock market crash: +12.94% (S&P 500: +5.81%)

2000 – Dot-com Bust: +5.83% (S&P 500: -9.03%)

2001 – Dot-com Bust: +3.76% (S&P 500: -11.85%)

2002 – Dot-com Bust: +14.31% (S&P 500: -21.97%)

2007 – Financial Meltdown: +12.43% (S&P 500: +5.48%)

2008 – Financial Meltdown: -8.36% (S&P 500: -36.55%)

2009 – Financial Meltdown: +19.08% (S&P 500: +25.94%)

2020 – Coronavirus Shutdown: +18.86% (S&P 500: +18.01%)

The Permanent Portfolio enabled investors to avoid losses during four critical financial downturns in the past 35 years. Imagine coming through the 1987 stock market crash, the dot-com bust, the 2008 financial meltdown, and the current COVID pandemic with gains in your portfolio?

The Three-Fund Portfolio

The Three-Fund Portfolio keeps things simple. You don’t need to spread your money across multiple asset classes to achieve the right mix of growth and safety. Instead, you’re more likely to outperform the market over the long term by investing in just three very broad-based funds.

Those three funds consist of:

- A domestic stock “total market” index fund

- An international stock “total market” index fund

- A bond, “total market” index fund

In that way, you’ll have exposure to broad domestic and international stocks and bonds. The use of index-based ETFs makes this easier to do than ever.

It isn’t a proper all-weather portfolio in the sense that it can turn positive returns during stock market crashes or periods of inflation or deflation. But because it’s heavily invested in times of stability and growth, the returns it will provide over the long term will generally exceed those of actual all-weather funds.

Should You Invest In the All-Weather Portfolio?

There’s no one portfolio or single investment strategy that’s right for all investors. But the basic concept of the All-Weather Portfolio is found in the name itself, all-weather. More specifically, you may want to consider that to be more of a reference to bad weather. The All-Weather Portfolio won’t outperform a growth-oriented portfolio over the long term and will even trail well behind it during times of stability and growth.

But the All-Weather Portfolio does something a growth-oriented portfolio won’t and probably can’t do; protect your portfolio during times of economic and financial crisis.

Based on the reality that times of economic and financial crisis are a certainty, maintaining an allocation in the All-Weather Portfolio seems like a smart strategy. The gains you’ll give up during the good times will be more than offset by the positive returns you’ll get during those times when you might ordinarily be losing money – and sleep.

Perhaps the best approach is to maintain allocations in an All-Weather Portfolio and a growth-oriented portfolio at all times. Much as a traditional investment portfolio sets allocations between stocks and bonds, you can decide what the allocation will be between all-weather and growth portfolios.

For example, you might choose a 60/40 split, with 60% invested in the growth portfolio and 40% in all-weather. You can even modify the allocations based on prevailing conditions.

The All-Weather Portfolio is another investment tool at your disposal, not an actual portfolio strategy.

The post Your Guide to the Ray Dalio All-Weather Portfolio appeared first on Best Wallet Hacks.

from Best Wallet Hacks https://ift.tt/3BiIqgw

Comments

Post a Comment

We will appreciate it, if you leave a comment.